how to save money on 50000 salary India

A ₹50,000 monthly salary sounds decent — and it is. But by the end of the month, most salaried employees in India find their bank account looking surprisingly thin. Rent, EMIs, groceries, petrol, Zomato orders, the occasional Amazon impulse buy… and suddenly, saving even ₹5,000 feels like a stretch.

If you’re wondering how to save money on 50000 salary India, the good news is — saving ₹10,000 a month is completely achievable — without living like a monk. You just need a plan, a few smart habits, and a clear picture of where your money is actually going.

In this guide, we break it all down — step by step, in plain English, with real Indian numbers. Let’s get into it.

Whether you’re a fresher or a mid-level professional, figuring out how to save money on 50000 salary India is one of the most searched financial questions — and for good reason. The strategies below are practical, tested, and designed for the Indian cost of living.

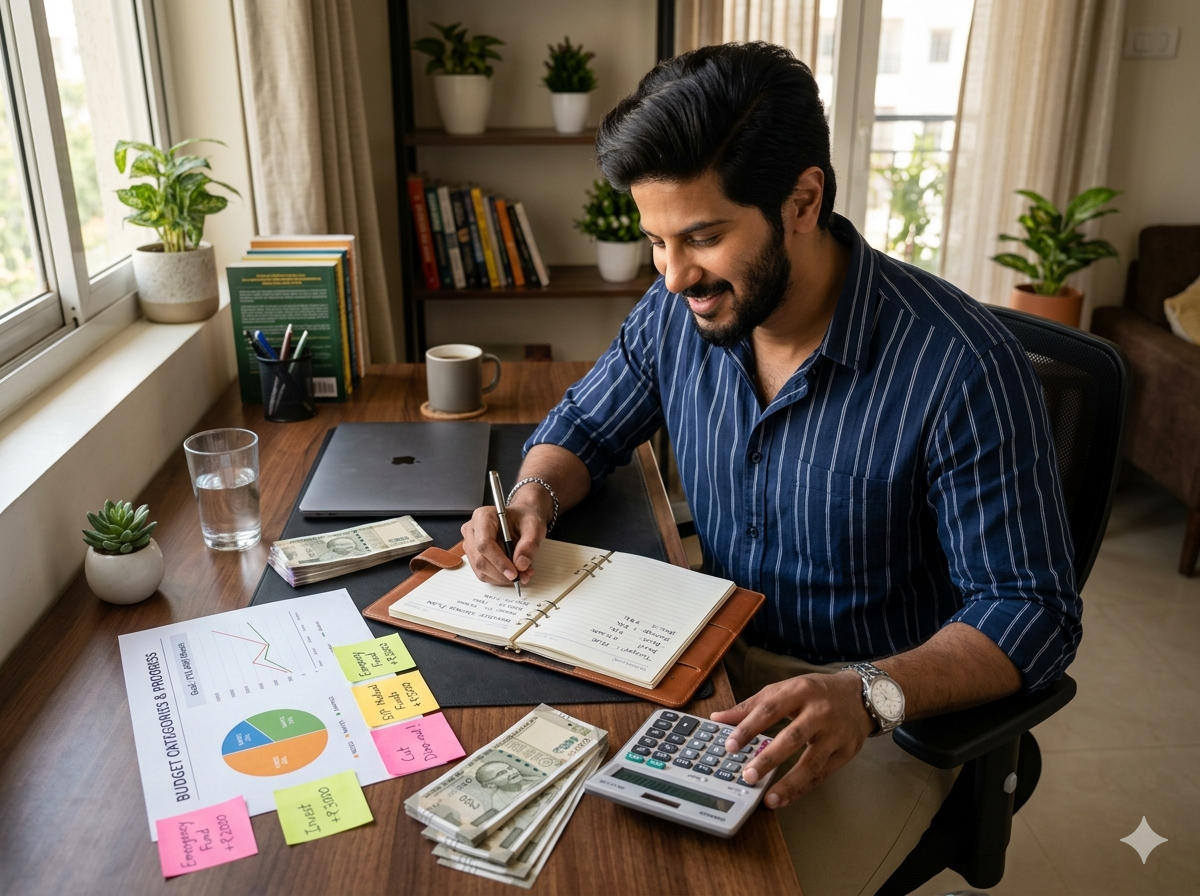

Meet Ananya — A Real Story That Might Sound Familiar

Meet Ananya, a 27-year-old HR executive from Pune who takes home ₹50,000 every month. On paper, she felt like she was doing okay. But every time she checked her savings account, the number barely moved.

She wasn’t splurging on luxury holidays. No designer bags, no fancy car. Just rent (₹12,000), groceries, her phone bill, a gym membership she barely used, weekend brunches with friends, and the occasional online shopping “treat.” Somehow, that was enough to swallow almost her entire salary.

After tracking her expenses for just one month using a simple Google Sheet, Ananya discovered she was spending ₹3,200 on food delivery alone. She was paying for two streaming subscriptions she had forgotten about. And her “emergency” credit card purchases were quietly adding ₹1,500 in monthly interest charges.

Ananya’s experience is exactly why so many people search for how to save money on 50000 salary India — because the answer isn’t about earning more, it’s about managing better. Six months later, after applying the exact steps we cover in this article, Ananya is consistently saving ₹11,000 every month — and investing ₹5,000 of that into mutual funds via a SIP (Systematic Investment Plan — a method of investing a fixed amount in mutual funds every month, like an automatic savings habit). Her story isn’t unique. Yours can look the same.

Step 1: Use the 50/30/20 Rule — But Make It Indian

The most reliable strategy for anyone learning how to save money on 50000 salary India is to start with a proven framework. The 50/30/20 rule says: spend 50% of your take-home on needs, 30% on wants, and save/invest 20%. For a ₹50,000 salary, that means saving ₹10,000 every single month — which is exactly our goal.

But the original rule was designed for Western salaries. In India, especially in metro cities, rent alone can eat 25–30% of your salary. So here’s a slightly tweaked version that works better for Indian salaried employees:

| Category | % of Salary | Amount (₹50,000) | What It Covers |

|---|---|---|---|

| Needs | 50% | ₹25,000 | Rent, groceries, transport, utilities, EMIs |

| Wants | 30% | ₹15,000 | Dining out, OTT, shopping, entertainment |

| Savings & Investments | 20% | ₹10,000 | Emergency fund, SIP, PPF, FD, RD |

The key trick: pay yourself first. On salary day, transfer ₹10,000 out immediately — into a separate savings account or start a SIP. Spend whatever’s left. This single habit is more powerful than any budgeting app.

Step 2: Find and Fix Your Money Leaks

The second step to understanding how to save money on 50000 salary India is identifying where your money silently disappears every month. Most people are shocked when they actually track their spending. Here are the most common money leaks (small, regular expenses that drain your wallet without you noticing) for Indian salaried employees:

🔴 The Big 5 Money Drains to Fix Right Now

- Food delivery apps (Zomato, Swiggy): The average Indian orders 8–12 times a month. At ₹300 per order, that’s ₹2,400–₹3,600 gone. Cooking even 4 extra meals at home saves ₹1,000+.

- Unused subscriptions: Netflix, Prime, Hotstar, Spotify, Gym, Newspaper apps — most people pay for 3–5 subscriptions they barely use. Audit them. Cancel the ones you haven’t opened in 30 days.

- Credit card interest: If you carry a balance on your HDFC, ICICI, or SBI credit card, you’re paying 36–42% annual interest. This is financial poison. Clear your balance before anything else.

- ATM and bank charges: Using another bank’s ATM costs ₹20–₹21 per transaction after the free limit. Small but avoidable. Use your own bank’s ATM or go cashless via UPI.

- Impulse online shopping: Weekend browsing + sale notifications = ₹1,500–₹3,000 in purchases you didn’t plan. The fix: add items to cart, wait 48 hours. Most cravings pass.

Step 3: A Practical ₹50,000 Monthly Budget That Actually Works

The most practical answer to how to save money on 50000 salary India is a real, city-adjusted budget — not just theory. Here’s a realistic month-by-month breakdown for a salaried employee in a mid-size Indian city (adjust rent for your city):

| Expense Category | Recommended Budget | Tips to Stay Within It |

|---|---|---|

| Rent / Housing | ₹10,000–₹12,000 | Consider PG or co-living if alone. Get HRA exemption from employer. |

| Groceries & Cooking | ₹4,000–₹5,000 | Weekly meal prep. Buy staples in bulk from Dmart or Jiomart. |

| Transport | ₹2,500–₹3,500 | Use metro/bus where available. Carpool with colleagues. |

| Utilities & Mobile | ₹1,500–₹2,000 | Switch to Jio/BSNL for affordable data. Track electricity usage. |

| Dining Out & Food Delivery | ₹2,000–₹2,500 | Set a hard monthly limit. Use Swiggy One only if it pays for itself. |

| Entertainment & OTT | ₹500–₹800 | Keep max 1–2 subscriptions. Share family plans with relatives. |

| Clothing & Personal Care | ₹1,500–₹2,000 | Shop during sale seasons only. Avoid fast fashion traps. |

| Miscellaneous / Buffer | ₹2,000 | Unspent buffer rolls into savings at month end. |

| 💰 Savings & Investment | ₹10,000 | Auto-transfer on salary day. Non-negotiable. |

Step 4: Don’t Just Save — Make Your ₹10,000 Work for You

Parking money in a regular savings account (earning just 3–4% interest) is better than spending it — but it’s not good enough. Inflation (the rise in prices over time) in India runs at about 5–6% annually, which means your savings account money is actually losing value in real terms.

Here’s how to split your ₹10,000 monthly savings smartly:

A Smart Split for Beginners

- ₹3,000 → Emergency Fund (Liquid Mutual Fund or SBI/HDFC High-Interest Savings Account): Build up 3–6 months of expenses as your safety net first. A liquid fund is a type of mutual fund where you can withdraw money within 24 hours — it earns more than a savings account (typically 6–7%).

- ₹5,000 → SIP in Equity Mutual Funds (via Zerodha Coin, Groww, or Paytm Money): Index funds or diversified equity funds historically return 11–14% annually over the long term. Start with a Nifty 50 index fund — it’s simple, low-cost, and regulated by SEBI (Securities and Exchange Board of India). You can track Nifty 50 performance on the NSE India official website.

- ₹2,000 → PPF or ELSS (for tax saving under Section 80C): PPF (Public Provident Fund) offers guaranteed 7.1% tax-free returns. ELSS (Equity Linked Savings Scheme) gives you tax deductions and potential for higher returns. Both reduce your income tax liability — saving you money twice over. PPF accounts can be opened at any nationalised bank or post office — current rates are published on the India Post official website.

Step 5: 6 Bonus Habits That Supercharge Your Savings

Beyond budgeting and investing, these six everyday habits can quietly add thousands to your monthly savings — without feeling deprived.

1. Use a Zero-Based Budget for One Month

A zero-based budget means every rupee of your ₹50,000 is assigned a job — savings, rent, food, transport — until ₹0 is “unaccounted for.” This doesn’t mean you spend it all. It means you decide where every rupee goes before the month starts. Apps like Walnut or even a simple Google Sheet work perfectly.

2. Claim All Your Tax Benefits

Most salaried employees in India leave thousands of rupees on the table every year. Make sure your employer is factoring in your HRA (House Rent Allowance — a tax exemption for rent you pay), LTA (Leave Travel Allowance), and Section 80C investments. At ₹50,000/month, smart tax planning can save you ₹10,000–₹18,000 per year. Use the official Income Tax India portal to calculate your exact tax liability and eligible deductions under Section 80C.

3. Switch to UPI for All Transactions

Paying in cash makes spending invisible. When you use UPI (Google Pay, PhonePe, BHIM), every transaction is recorded and visible. This alone increases mindfulness and reduces impulse spending for most people by 15–20%.

4. Use Cashback Credit Cards Wisely

Cards like the HDFC Millennia or SBI SimplySAVE offer 1–5% cashback on everyday spends. The rule: use the card for planned purchases only, and pay the full bill on or before the due date every single month. Never pay just the minimum due — that’s how the credit card trap starts.

5. Cook at Least 5 Days a Week

Food is the single most controllable expense in a young Indian salaried professional’s budget. Cooking at home 5 days a week, even simple dal-chawal and roti sabzi, cuts your food costs by 50–60% compared to daily ordering. Meal prep on Sundays for the week ahead — it saves time and money.

6. Start an “Anti-Budget” Savings Jar

Every time you resist a purchase you were tempted by — a gadget, an outfit, a food order — transfer that exact amount to a separate savings goal. Bought a ₹499 jacket on Myntra? Nope — transfer ₹499 instead. This gamifies saving and makes it feel rewarding.

Your Personalised Monthly Budget Planner

Use this free planner — built specifically for those asking how to save money on 50000 salary India — to see your real savings potential in seconds. Enter your income and monthly expenses below.

Quick Recap: Your ₹10,000/Month Savings Roadmap

Here’s everything we covered in this guide on how to save money on 50000 salary India, condensed into one simple action plan:

- ✅ Day 1 of every month: Auto-transfer ₹10,000 to a separate savings account — before you spend a rupee.

- ✅ This week: Track every expense for 7 days. Identify your top 2 money leaks.

- ✅ This month: Cancel unused subscriptions. Reduce food delivery to max 4 orders/week.

- ✅ This month: Start a ₹5,000 SIP in a Nifty 50 index fund via Zerodha, Groww, or your bank’s app.

- ✅ This year: Invest ₹2,000/month in PPF or ELSS to reduce tax and build long-term wealth.

- ✅ Always: Pay your credit card bill in full every month. Never carry a balance.

Frequently Asked Questions

How can I save ₹10,000 per month on a ₹50,000 salary in India?

Apply the 50/30/20 rule: spend ₹25,000 on needs, ₹15,000 on wants, and save ₹10,000. Transfer your savings on salary day before spending. Cut food delivery, cancel unused subscriptions, and avoid carrying a credit card balance. These four steps alone free up ₹10,000 for most people.

Where should I invest ₹10,000 per month in India?

A simple split: ₹3,000 into a liquid fund as emergency savings, ₹5,000 into a Nifty 50 index fund SIP via Groww or Zerodha, and ₹2,000 into PPF or ELSS for tax benefits under Section 80C. Adjust once your emergency fund covers 3–6 months of expenses.

Is ₹50,000 salary enough to save in India?

Yes — saving 15–20% (₹7,500–₹10,000) on ₹50,000 is achievable for most Indian salaried employees. It depends on your city and lifestyle, but tracking expenses and paying yourself first makes it realistic even in metros like Bengaluru or Mumbai with smart budgeting.

How can I save tax on a ₹50,000 monthly salary?

On a ₹6 lakh annual salary, claim Section 80C deductions up to ₹1.5 lakh via PPF, ELSS, or EPF. Use HRA exemption if you pay rent. The standard deduction for salaried employees is ₹75,000 (FY2024-25 new regime). Consult a CA for your exact tax liability.

Should I start a SIP on a ₹50,000 salary?

Yes — start with ₹3,000–₹5,000/month in a Nifty 50 index fund. Increase it by 10% each year (step-up SIP) as your salary grows. Consistency and time in the market matter far more than the amount you start with.

What should I do first — clear debt or start saving?

Clear high-interest debt first (credit card balances at 36–42%, personal loans above 18%). Once done, build a ₹50,000–₹1 lakh emergency fund, then begin investing. Low-interest debt like home loans can coexist with a SIP.

What is the best budgeting app for Indians to track expenses?

Walnut (auto-reads SMS), Money Manager, and Jupiter are popular options in India. Even a free Google Sheet with 5 columns (date, category, amount, mode, notes) works beautifully and keeps you in full control of your financial data.