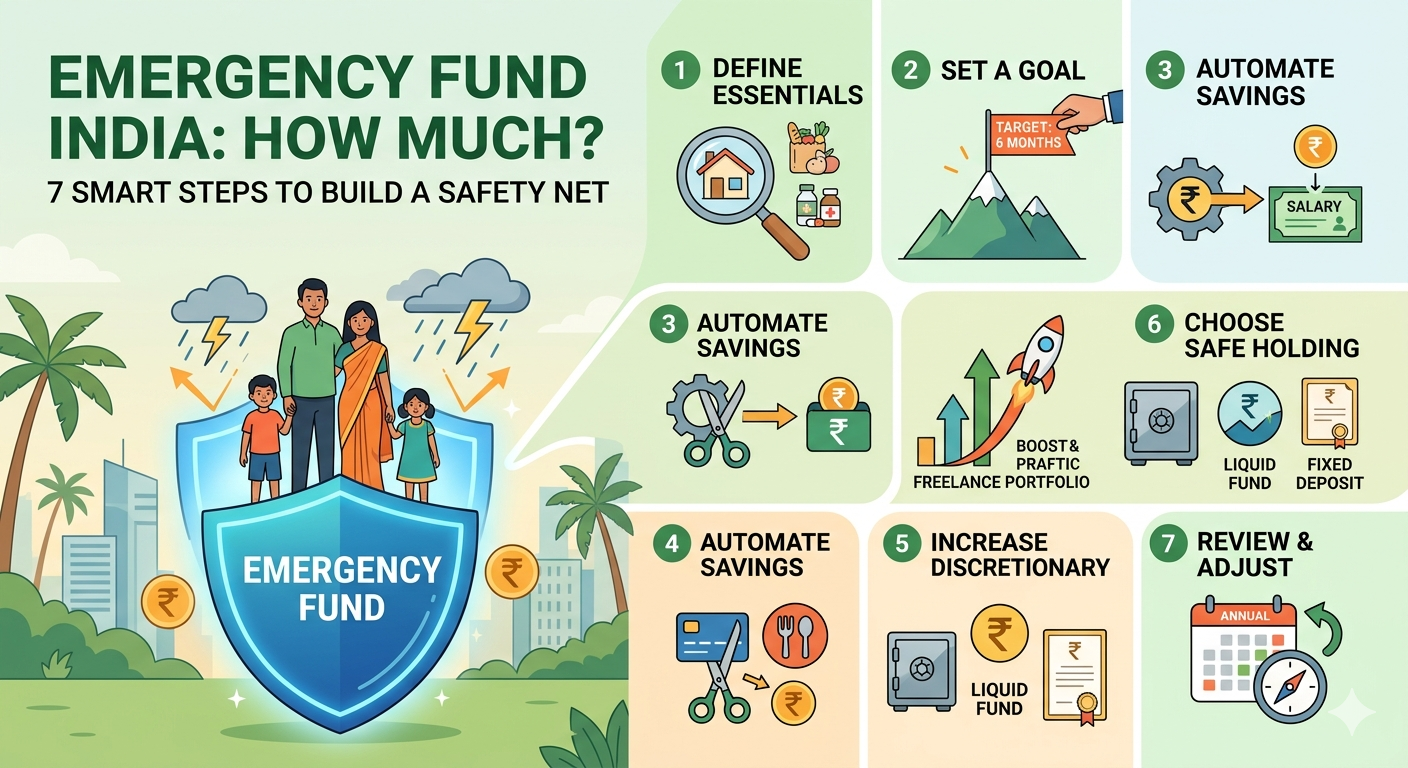

Emergency Fund India How Much: 7 Smart Steps to Build a Safety Net

If you are wondering emergency fund In India how much you should save, the short answer is this: enough to cover your essential expenses for at least 3 to 12 months.

That number depends on your job, family size, and monthly costs. For Indian salaried employees, an emergency fund is one of the most important parts of personal finance because it protects you from medical bills, job loss, and sudden family expenses.

In this guide, you will learn how to build emergency fund India step by step, with practical examples, Indian context, and simple action points you can use today.

What An Emergency Fund Really Is

An emergency fund is money kept aside only for unexpected situations. It is not for shopping, travel, or planned purchases.

Think of it as a financial first-aid kit. If your salary stops for a while or you face a medical emergency, this money helps you stay afloat without taking expensive loans.

For Indian households, this matters even more because many families support parents, children, EMIs, and health costs at the same time.

Emergency Fund In India How Much To Save

The easiest rule is to save 3 to 12 months of essential expenses. That is the most practical way to answer emergency fund in India how much for your situation.

If you are single with a stable job, 3 months may be enough. If you are married, have dependents, or work in a variable-income role, 6 to 12 months is safer.

| Monthly Essential Expenses | 3 Months | 6 Months | 12 Months |

|---|---|---|---|

| ₹30,000 | ₹90,000 | ₹1.8 lakhs | ₹3.6 lakhs |

| ₹50,000 | ₹1.5 lakhs | ₹3 lakhs | ₹6 lakhs |

| ₹75,000 | ₹2.25 lakhs | ₹4.5 lakhs | ₹9 lakhs |

The best formula is simple: essential monthly expenses multiplied by the number of months you need. Do not use your full salary if your salary includes spending that can be reduced.

A good emergency savings India target should be realistic, not scary. Start with a smaller goal first, then grow it step by step.

A Simple Indian Example

Meet Neha, a 29-year-old HR executive from Pune who earns ₹78,000 a month. She used to think saving was only for retirement, not emergencies.

When her father needed an urgent hospital procedure, she had to borrow money because she had no emergency fund. That experience changed her mindset completely.

Today, she saves ₹8,000 every month and is slowly building 6 months of expenses. Her story is a reminder that how to build emergency fund India is not theory — it is a practical life skill.

How To Build Emergency Fund In India Step By Step

Step 1: List Your Essential Expenses

Write down only the things you must pay every month. Include rent, groceries, electricity, transport, school fees, insurance, and EMIs.

Do not include lifestyle spending like Amazon shopping, weekend outings, or expensive subscriptions. The goal is to know your true survival number.

Step 2: Pick Your Month Target

This is where how many months salary emergency fund becomes useful. A salaried employee with a secure role may choose 3 months, while a family with dependents may choose 6 months or more.

If your industry is unstable or your income changes often, 9 to 12 months gives better protection.

Step 3: Open A Separate Account

Keep the fund in a separate savings account so it does not mix with monthly spending money. This makes your money easier to track and harder to spend carelessly.

Banks like SBI, HDFC, ICICI, and IDFC FIRST are commonly used by Indian savers. The key is not just the bank name, but the discipline of keeping the money untouched.

Step 4: Automate Monthly Transfers

Set an auto-transfer from salary day to your emergency account. Even ₹3,000 to ₹10,000 every month can build a strong fund over time.

Automation removes the temptation to spend first and save later. That small system change is often the difference between progress and delay.

Step 5: Use Safe Parking Options

Your emergency fund should be easy to access. Good options include savings accounts, fixed deposits, and liquid mutual funds, which are designed for short-term parking.

According to common emergency fund guidance in India, a mix of savings account, FD, and liquid funds gives both safety and decent returns [web:1][web:23].

Step 6: Build In Small Milestones

Do not wait until you can save the full target. First aim for ₹50,000, then one month of expenses, then three months. Small wins keep you motivated.

If you receive a bonus, tax refund, or freelance payment, add a part of it to the fund. That speeds up the process without hurting your monthly budget.

Step 7: Review Once A Year

Inflation changes your needs over time. What felt enough two years ago may not be enough today, especially if rent, school fees, or EMIs have gone up.

Review your fund every year and top it up if needed. This keeps your emergency savings India plan aligned with real life.

Emergency Fund Calculator

Emergency Fund in India How Much Calculator

This calculator gives you a fast estimate of emergency fund In India how much to keep aside.

Where To Keep The Money

For an emergency fund in india, safety and liquidity matter more than high returns. That is why savings accounts, liquid mutual funds, and short-term fixed deposits are the most sensible choices.

| Option | Access | Typical Use |

|---|---|---|

| Savings Account | Instant | First layer of safety |

| Fixed Deposit | 1 to 7 days | Medium-term parking |

| Liquid Mutual Fund | Usually 1 day | Balance of safety and return |

According to emergency fund in India, a smart mix of savings account, FD, and liquid funds can work well for most households [web:1][web:23][web:50].

The goal is not maximum return. The goal is fast access, low risk, and enough money to survive the emergency without borrowing.

Frequently Asked Questions

How much emergency fund should I keep in India?

Most salaried Indians should keep 3 to 6 months of essential expenses. If your income is unstable or you support dependents, 9 to 12 months is better.

How do I build an emergency fund on a low salary?

Start with a small monthly amount like ₹2,000 or ₹5,000 and automate it. Build the first ₹50,000 target before moving to a bigger goal.

Where should I keep my emergency savings India?

Keep it in a savings account, short-term FD, or liquid mutual fund. Choose something safe and easy to access within a day or two.

Is 6 months salary enough for an emergency fund?

For many Indian families, yes. But the better rule is to look at essential expenses, not salary, because salary and spending are not always the same.

Can I invest my emergency fund in mutual funds?

Use only liquid or overnight funds if you want very low risk. Avoid equity funds because they can fall in value when you need the money most.

How often should I review my emergency fund?

Review it once a year or after a major life change like marriage, a child, a job switch, or a rise in expenses.